Financial Terms And Simple Calculations

|

Specification:

3.2 Financial Terms and Simple Calculations • basic financial terms • calculating profit and loss |

Candidates need to understand the terms:

price, sales, revenue, costs and profit and the relationship between these. Candidates should be able to perform simple calculations based on these figures to determine profit/loss. |

Financial Terms

Learning Objectives:

- To understand the financial terms a new business needs to use (D-E)

- To be able to calculate the costs a business faces and whether it has made a profit or loss (B-C)

- To evaluate what this data means (A*-A)

- To understand the financial terms a new business needs to use (D-E)

- To be able to calculate the costs a business faces and whether it has made a profit or loss (B-C)

- To evaluate what this data means (A*-A)

| financial_terms_worksheet.doc |

Starter Activity: Think about an average month for you. Write down where all the money you receive comes from, and write down everything you spend it on. If you can, write down the approximate amounts.

Price:

This is the amount a business asks customers to pay for a single product.

This can be guided by competitor's prices or the cost of making the good.

If a product is popular, businesses may increase prices (WHAT ECONOMICAL TERM IS THIS?)

If a business has goods left over, they may lower prices (WHAT ECONOMICAL TERM IS THIS?)

This is the amount a business asks customers to pay for a single product.

This can be guided by competitor's prices or the cost of making the good.

If a product is popular, businesses may increase prices (WHAT ECONOMICAL TERM IS THIS?)

If a business has goods left over, they may lower prices (WHAT ECONOMICAL TERM IS THIS?)

Sales:

This is the number of products sold by a business over a time period (days/months/years).

Sales are given as the number sold, not in terms of the money made.

This is the number of products sold by a business over a time period (days/months/years).

Sales are given as the number sold, not in terms of the money made.

Revenue (Income/Turnover):

This is the income received from selling the good or service.

Revenue is worked out by using the following calculation:

REVENUE = SELLING PRICE x SALES (number of products sold)

This is the income received from selling the good or service.

Revenue is worked out by using the following calculation:

REVENUE = SELLING PRICE x SALES (number of products sold)

Costs:

These are the costs necessary to set up and run the business.

These can be fixed costs and variable costs.

Fixed costs do not alter when a business changes its output.

Variable costs vary directly with the business's level of output and sales.

TOTAL COSTS = FIXED COSTS + VARIABLE COSTS

Costs can also be divided up into start-up costs and running costs.

Start-up costs will have to be paid when the business is launched:

These are the costs necessary to set up and run the business.

These can be fixed costs and variable costs.

Fixed costs do not alter when a business changes its output.

Variable costs vary directly with the business's level of output and sales.

TOTAL COSTS = FIXED COSTS + VARIABLE COSTS

Costs can also be divided up into start-up costs and running costs.

Start-up costs will have to be paid when the business is launched:

- Buildings

- Machinery and equipment

- Market research

- Rent

- Materials

- Wages

- Taxes

Profit:

Profit is the amount that a business's revenue from sales exceeds its costs.

Loss is the amount by which a business's costs exceed its revenue.

Where revenue equals costs, a business has BROKEN EVEN.

PROFITS (OR LOSSES) = REVENUE - TOTAL COSTS

Profit is the amount that a business's revenue from sales exceeds its costs.

Loss is the amount by which a business's costs exceed its revenue.

Where revenue equals costs, a business has BROKEN EVEN.

PROFITS (OR LOSSES) = REVENUE - TOTAL COSTS

Plenary:

Do you think a new business will always look to make a profit in it's first year?

Is this possible?

What document will contain all a business's projections as to how much profit it thinks it will make?

Which stakeholders will be interested in how much profit (or loss) a business is making?

Do you think a new business will always look to make a profit in it's first year?

Is this possible?

What document will contain all a business's projections as to how much profit it thinks it will make?

Which stakeholders will be interested in how much profit (or loss) a business is making?

Financial Calculations

Learning Objectives:

- To understand how to calculate revenue, total costs and profit or loss (D-E)

- To be able to analyse the importance of understanding these figures (B-C)

- To be able to evaluate these figures and recommend financial decisions (A*-A)

- To understand how to calculate revenue, total costs and profit or loss (D-E)

- To be able to analyse the importance of understanding these figures (B-C)

- To be able to evaluate these figures and recommend financial decisions (A*-A)

Starter Activity: What is the difference between fixed and variable costs? How many of each can you list?

Calculating Revenue:

REVENUE = SELLING PRICE x NUMBER OF PRODUCTS SOLD

REVENUE = SELLING PRICE x NUMBER OF PRODUCTS SOLD

Calculating Total Costs:

TOTAL COSTS = FIXED COSTS + VARIABLE COSTS

TOTAL COSTS = FIXED COSTS + VARIABLE COSTS

Calculating Profits:

PROFIT (OR LOSS) = REVENUE - TOTAL COSTS

PROFIT (OR LOSS) = REVENUE - TOTAL COSTS

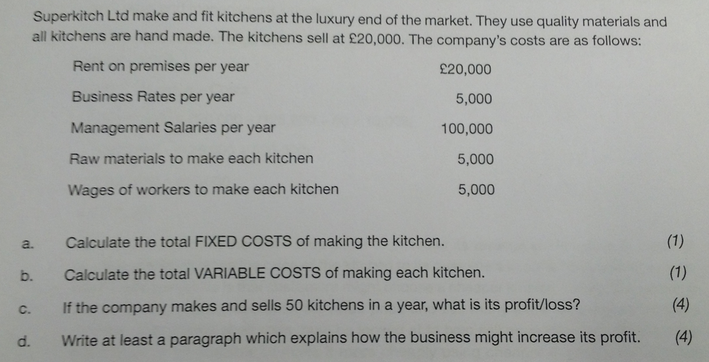

For question d), explain the advantages and disadvantages of each option.

Using this information:

Later on in the course, you will need to make judgements based on financial information for how a business should act in the future. Using the information above, the company have decided that they want a loan of £500,000 to help them expand. Which source of finance do you think they should use and why? (9 marks)

Using this information:

Later on in the course, you will need to make judgements based on financial information for how a business should act in the future. Using the information above, the company have decided that they want a loan of £500,000 to help them expand. Which source of finance do you think they should use and why? (9 marks)

Plenary: Does the company with the most profit always have the most successful business?

Homework: Research 2 businesses in the news. One needs to have made a profit and one needs to have made a loss. Explain why you think this?

Homework: Research 2 businesses in the news. One needs to have made a profit and one needs to have made a loss. Explain why you think this?